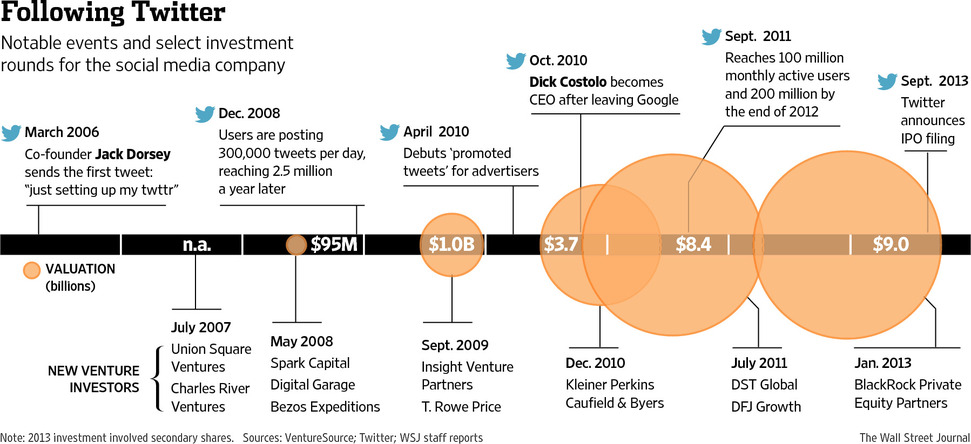

Some cool infographics from the WSJ in honor of Twitter finally revealing their S-1

Some cool infographics from the WSJ in honor of Twitter finally revealing their S-1

Great list of quotes from Henry Ford. Go check out the full article 21 Quotes From Henry Ford On Business, Leadership And Life over at Forbes.

A great article by Jason Zweig about the one and only Charlie Munger. Link (paywall)

As usual, a few highlights:

“Trained as a meteorologist at the California Institute of Technology, Mr. Munger thinks in terms of probabilities rather than certainties, say those who know him well. An early divorce and the death of his young son from leukemia taught Mr. Munger that adversity provides an opportunity to show what you are made of. Decades of voracious reading in history, science, biography and psychology have made him an acute diagnostician of human folly.”

My favorite piece of advice in the article:

“Mr. Munger favors what he calls “sitting on your a—,” regardless of what the investing crowd is doing, until a good investment finally materializes.”

“Many money managers spend their days in meetings, riffling through emails, staring at stock-quote machines with financial television flickering in the background, while they obsess about beating the market. Mr. Munger and Mr. Buffett, on the other hand, ‘sit in a quiet room and read and think and talk to people on the phone,’ says Shane Parrish, a money manager who edits Farnam Street, a compelling blog about decision making. ‘By organizing their lives to tune out distractions and make fewer decisions,’ he adds, Mr. Munger and Mr. Buffett “have tilted their odds toward making better decisions’.”

Source: WSJ

Buffett on Career Risk:

“Wall Street abhors a commercial vacuum. If the will to believe stirs within the customer, the merchandise will be supplied – without warranty. When franchise companies are wanted by investors, franchise companies will be found – and recommended by the underwriters. If there are none to be found, they will be created. Similarly, if above-average investment performance is sought, it will be promised in abidance – and at least the illusion will be produced.

Initially those who know better will resist promising the impossible. As the clientele first begins to drain away, advisors will argue the un-soundness of the new trend and the strengths of the old methods. But when the trickle gives signs of turning into a flood, business Darwinism will prevail and most organizations will adapt. This is what happened in the money management field.”

Buffett on how to manage a portfolio (in this case the Washington Post’s Pension):

“(5) My final option – and the one to which I lean, although not at anything like a 45-degree angle – is mildly unconventional, thereby causing somewhat more legal risk for directors. It may differ from other common stock programs, more in attitude than in appearance, or even results. It involves treating portfolio management decisions much like business acquisition decisions by corporate managers.

The directors and officers of the company consider themselves to be quite capable of making business decisions, including decisions regarding the long-term attractiveness of specific business operations purchased at specific prices. We have made decisions to purchase several television businesses, a newspaper business, etc. And in other relationships we have made such judgments covering a much wider spectrum of business operations.

Negotiated prices for such purchases of entire businesses often are dramatically higher than stock market valuations attributable to well-managed similar operations. Longer term, rewards to owners in both cases will flow from such investments proportional to the economic results of the business. By buying small pieces of businesses through the stock market rather than entire businesses through negotiation, several disadvantages occur: (a) the right to manage, or select mangers, is forfeited; (b) the right to determine dividend policy or direct the areas of internal investment is absent; (c) ability to borrow long-term against the business assets (versus against the stock position) is greatly reduced; and (d) the opportunity to sell the business on a full-value, private-owner basis is forfeited.

These are important negative factors but, if a group of investments are carefully chosen at a bargain price, it can minimize the impact of a single bad experience, in say, the management area, which cannot be corrected. And occasionally there is an offsetting advantage which can be of very substantial value – but for which nothing should be paid at the time of purchase. That relates to the periodic tendency of stock markets to experience excesses which cause businesses – when changing hands in small pieces through stock transactions – to sell at prices significantly above privately-determine negotiated values. At such times, holdings may be liquidated at better prices than if the whole business were owned – and, due to the impersonal nature of securities markets, no moral stigma need be attached to dealing with such unwitting buyers.

Stock market prices may bounce wildly and irrationally but, if decisions regarding internal rates of return of the business are reasonably correct – and a small portion of the business is bought at a fraction of its private-owner value – a good return for the fund should be assured over the time span against which pension fund results should be measured.

It might be asked what the difference is between this approach and simply pick stocks a la Morgan, Scudder, Stevens, etc. It is, in large part, a matter of attitude, whereby the results of the business become the standard against which measurements are made rather than quarterly stock prices. It embodies a long time span for judgement confirmation, just as does an investment by a corporation in a major new division, plant or product. It treats stock ownership as business ownership with the corresponding adjustment in mental set. And it demands an excess of value over price paid, not merely a favorable short-term earnings or stock market outlook. General stock market considerations simply don’t enter into the purchase decision.

Finally, it rests on a belief, which both seems logical and which has been borne out historically in securities markets, that intrinsic business value is the eventual prime determinant of stock prices. In the words of my former boss: ‘in the short run the market is a voting machine, but in the long run it is a weighing machine.'”

A nice analysis of moats by Credit Suisse. Report embedded below – followed by Buffett’s quotes on moats. Note the Value Creation Checklist on p. 52 of the analysis.

Warren Buffett on Economic Moats

“What we refer to as a “moat” is what other people might call competitive advantage . . . It’s something

that differentiates the company from its nearest competitors – either in service or low cost or taste or

some other perceived virtue that the product possesses in the mind of the consumer versus the next best alternative . . . There are various kinds of moats. All economic moats are either widening or narrowing – even though you can’t see it.”

— Outstanding Investor Digest, June 30, 1993

“Look for the durability of the franchise. The most important thing to me is figuring out how big a moat there is around the business. What I love, of course, is a big castle and a big moat with piranhas and crocodiles.”

— Linda Grant, “Striking Out at Wall Street,” U.S. News & World Report, June 12, 1994

“The key to investing is not assessing how much an industry is going to affect society, or how much it will grow, but rather determining the competitive advantage of any given company and, above all, the

durability of that advantage. The products or services that have wide, sustainable moats around them are the ones that deliver rewards to investors.”

— Warren Buffett and Carol Loomis, “Mr. Buffett on the Stock Market,” Fortune, November 22, 1999

We think of every business as an economic castle. And castles are subject to marauders. And in

capitalism, with any castle . . . you have to expect . . . that millions of people out there . . . are thinking

about ways to take your castle away. Then the question is, “What kind of moat do you have around that castle that protects it?”

— Outstanding Investor Digest, December 18, 2000

“When our long-term competitive position improves . . . we describe the phenomenon as “widening the moat.” And doing that is essential if we are to have the kind of business we want a decade or two from now. We always, of course, hope to earn more money in the short-term. But when short-term and longterm conflict, widening the moat must take precedence. ”

— Berkshire Hathaway Letter to Shareholders, 2005

“A truly great business must have an enduring “moat” that protects excellent returns on invested capital. The dynamics of capitalism guarantee that competitors will repeatedly assault any business “castle” that is earning high returns . . . Our criterion of “enduring” causes us to rule out companies in industries prone to rapid and continuous change. Though capitalism’s “creative destruction” is highly beneficial for society, it precludes investment certainty. A moat that must be continuously rebuilt will eventually be no moat at all . . . Additionally, this criterion eliminates the business whose success depends on having a great manager.”

— Berkshire Hathaway Letter to Shareholders, 2007

Found via Punchcard Investing Blog

Seth_Klarman_Views_(24_pgs) June 2013

I’ve been meaning to read this for a while – I can’t remember where I came across this or who I owe credit to for originally posting this but thank you. This is probably the best piece I’ve read all summer, maybe all year.

For this blog post I originally started jotting down excerpts from this speech that resonated with me. I quickly realized that I was writing down everything – literally re-transcribing the entire speech. I would have copied and pasted the whole thing for you, dear reader, but this appears to be a scanned copy of a printed document.

Anyway, give it a read – don’t be daunted by the 24 pages, it’s actually a very quick read and it is well worth your time.

Enjoy.

Great infographic from the folks and Funders and Founders:

Fascinating peek into Tesla’s factory.

Source: Wired

An oldie but a goodie from James Montier, back when he was with Dresdner Kleinwort Wasserstein.

Montier outlines the seven sins:

Honorable mention: the illusion of control, the possibility of having too much choice, and benchmarking

Montier provides a brief summary on each of these sins but goes on to dedicate a chapter to each:

This collection of notes aims to explore some of the more obvious behavioural weaknesses inherent in the ‘average’ investment process.

► Seven sins (common mistakes) were identified. The first was placing forecasting at the very heart of the investment process. An enormous amount of evidence suggests that investors are generally hopeless at forecasting. So using forecasts as an integral part of the investment process is like tying one hand behind your back before you start.

► Secondly, investors seem to be obsessed with information. Instead of focusing on a few important factors (such as valuations and earnings quality), many investors spend countless hours trying to become experts about almost everything. The evidence suggests that in general more information just makes us increasingly over-confident rather than better at making decisions.

► Thirdly, the insistence of spending hours meeting company managements strikes us as bizarre from a psychological standpoint. We aren’t good at looking for information that will prove us to be wrong. So most of the time, these meetings are likely to be mutual love ins. Our ability to spot deception is also very poor, so we won’t even spot who is lying.

► Fourthly, many investors spend their time trying to ‘beat the gun’ as Keynes put it. Effectively, everyone thinks they can get in at the bottom and out at the top. However, this seems to be remarkably hubristic.

► Fifthly, many investors seem to end up trying to perform on very short time horizons and overtrade as a consequence. The average holding period for a stock on the NYSE is 11 months! This has nothing to do with investment, it is speculation, pure and simple.

► Penultimately, we all appear to be hardwired to accept stories. However, stories can be very misleading. Investors would be better served by looking at the facts, rather than getting sucked into a great (but often hollow) tale.

► And finally, many of the decisions taken by investors are the result of group interaction. Unfortunately groups are far more a behavioural panacea. In general, they amplify rather than alleviate the problems of decision making.

► Each of these sins seems to be a largely self imposed handicap when it comes to trying to outperform. Identifying the psychological flaws in the ‘average’ investment process is an important first step in trying to design a superior version that might just be more robust to behavioural biases.