Cool chart from Quartz that helps visualize unemployment rates and what’s included / not included in the official unemployment rate and the broader, U6 measure:

Cool chart from Quartz that helps visualize unemployment rates and what’s included / not included in the official unemployment rate and the broader, U6 measure:

There is a great article about Warren Buffett’s approach to investing from The American Association of Independent Investors (link). The article is from January 1998 but the advice is timeless. Below is a summary of his approach. The article itself is a quick and easy read, well worth your time.

The Warren Buffett Approach

Philosophy and style

Investment in stocks based on their intrinsic value, where value is measured by the ability to generate earnings and dividends over the years. Buffett targets successful businesses—those with expanding intrinsic values, which he seeks to buy at a price that makes economic sense, defined as earning an annual rate of return of at least 15% for at least five or 10 years.

Universe of stocks

No limitation on stock size, but analysis requires that the company have been in existence for a considerable period of time.

Criteria for initial consideration

Consumer monopolies, selling products in which there is no effective competitor, either due to a patent or brand name or similar intangible that makes the product unique. In addition, he prefers companies that are in businesses that are relatively easy to understand and analyze, and that have

the ability to adjust their prices for inflation.

Other factors

• A strong upward trend in earnings

• Conservative financing

• A consistently high return on shareholder’s equity

• A high level of retained earnings

• Low level of spending needed to maintain current operations

• Profitable use of retained earnings

Valuing a Stock

Buffett uses several approaches, including:

Stock monitoring and when to sell

Does not favor diversification; prefers investment in a small number of companies that an investor can know and understand extensively. Favors holding for the long term as long as the company remains “excellent”—it is consistently growing and has quality management that operates for the benefit of shareholders. Sell if those circumstances change, or if an alternative investment offers a better return.

On Sunday the NYT ran an interesting op-ed by former Congressmen and Reagan’s budget director, David Stockman. The article has an extremely pessimistic outlook for our country and economy; you might even think you were reading Zero Hedge and not the NYT (the only difference is Stockman recommends holding cash as opposed to gold).

He highlights some huge problems facing our nation – the most discouraging is our government’s inability to do anything about them. Below are a few paragraphs that sum things up. The whole article is worth your time and attention (link).

The future is bleak. The greatest construction boom in recorded history — China’s money dump on infrastructure over the last 15 years — is slowing. Brazil, India, Russia, Turkey, South Africa and all the other growing middle-income nations cannot make up for the shortfall in demand. The American machinery of monetary and fiscal stimulus has reached its limits. Japan is sinking into old-age bankruptcy and Europe into welfare-state senescence. The new rulers enthroned in Beijing last year know that after two decades of wild lending, speculation and building, even they will face a day of reckoning, too.

THE state-wreck ahead is a far cry from the “Great Moderation” proclaimed in 2004 by Mr. Bernanke, who predicted that prosperity would be everlasting because the Fed had tamed the business cycle and, as late as March 2007, testified that the impact of the subprime meltdown “seems likely to be contained.” Instead of moderation, what’s at hand is a Great Deformation, arising from a rogue central bank that has abetted the Wall Street casino, crucified savers on a cross of zero interest rates and fueled a global commodity bubble that erodes Main Street living standards through rising food and energy prices — a form of inflation that the Fed fecklessly disregards in calculating inflation.

These policies have brought America to an end-stage metastasis. The way out would be so radical it can’t happen. It would necessitate a sweeping divorce of the state and the market economy. It would require a renunciation of crony capitalism and its first cousin: Keynesian economics in all its forms. The state would need to get out of the business of imperial hubris, economic uplift and social insurance and shift its focus to managing and financing an effective, affordable, means-tested safety net.

All this would require drastic deflation of the realm of politics and the abolition of incumbency itself, because the machinery of the state and the machinery of re-election have become conterminous. Prying them apart would entail sweeping constitutional surgery: amendments to give the president and members of Congress a single six-year term, with no re-election; providing 100 percent public financing for candidates; strictly limiting the duration of campaigns (say, to eight weeks); and prohibiting, for life, lobbying by anyone who has been on a legislative or executive payroll. It would also require overturning Citizens United and mandating that Congress pass a balanced budget, or face an automatic sequester of spending.

It would also require purging the corrosive financialization that has turned the economy into a giant casino since the 1970s. This would mean putting the great Wall Street banks out in the cold to compete as at-risk free enterprises, without access to cheap Fed loans or deposit insurance. Banks would be able to take deposits and make commercial loans, but be banned from trading, underwriting and money management in all its forms.

It would require, finally, benching the Fed’s central planners, and restoring the central bank’s original mission: to provide liquidity in times of crisis but never to buy government debt or try to micromanage the economy. Getting the Fed out of the financial markets is the only way to put free markets and genuine wealth creation back into capitalism.

That, of course, will never happen because there are trillions of dollars of assets, from Shanghai skyscrapers to Fortune 1000 stocks to the latest housing market “recovery,” artificially propped up by the Fed’s interest-rate repression. The United States is broke — fiscally, morally, intellectually — and the Fed has incited a global currency war (Japan just signed up, the Brazilians and Chinese are angry, and the German-dominated euro zone is crumbling) that will soon overwhelm it. When the latest bubble pops, there will be nothing to stop the collapse. If this sounds like advice to get out of the markets and hide out in cash, it is.

No commentary necessary.

Found via The Big Picture

Below are a few excerpts from Tim Duy’s article about the strength of the economic recovery. Go check out the full article, charts included, here.

The economy has proved to be very resilient. We have weathered external demand shocks, external financial crises, and even fiscal contraction, and all the while economic activity continued to grind higher. Looking back, it seems that the biggest risk the economy faced was the Fed’s start/stop approach to quantitative easing. That problem appears solved with open-ended QE linked to economic guideposts.

At the risk of sounding overly optimistic, I am going to go out on a limb: The recovery is here to stay. Not “stay” as in “permanent.” I am not predicting the end of the business cycle. But “stay” until some point after the Federal Reserve begins to raise interest rates, which I don’t expect until 2015. This doesn’t mean you need to be happy about the pace of growth. But it does mean that a US recession in the next three years should be pretty far down on your list of concerns.

His take is based on strength in (1) industrial production, (2) retail sales, (3) the housing market, and (4) employment.

What does this mean for the market? Good question, nobody can be sure – but its certainly possible to see equities contract while the underlying economy continues to improve. Just read the previous posts highlighting John Hussman’s bearish take on the markets. Whatever the markets do, lets hope the economic recovery stays intact and at least provides a buoy should Mr. Market freak out.

Also, lets take into account the forward looking nature of equities, after all any real investor worrying about fundamentals should be thinking a minimum of 3-5 years out (despite the majority of Wall Street focusing on the next quarter or two). This will put fundamental / value investors in the uncomfortable position of factoring in the Fed’s exit well ahead of the rest of the market, if not already.

Tim’s bottom line:

Bottom Line: The US economy is less fragile than commonly believed; it has endured a series of shocks over the last three years without major incident. I am claiming neither that equity prices won’t stumble, nor that we should be happy with the pace of activity. But I do think that a recession is unlikely before the Federal Reserve begins raising interest rates – something not likely to happen for two years. While long-run predictions are dangerous, for the sake of argument add up to another two years for tighter policy to reverberate through the economy and you are looking at sometime around 2016/2017 when the next recession hits. That’s the timeframe I am currently thinking about.

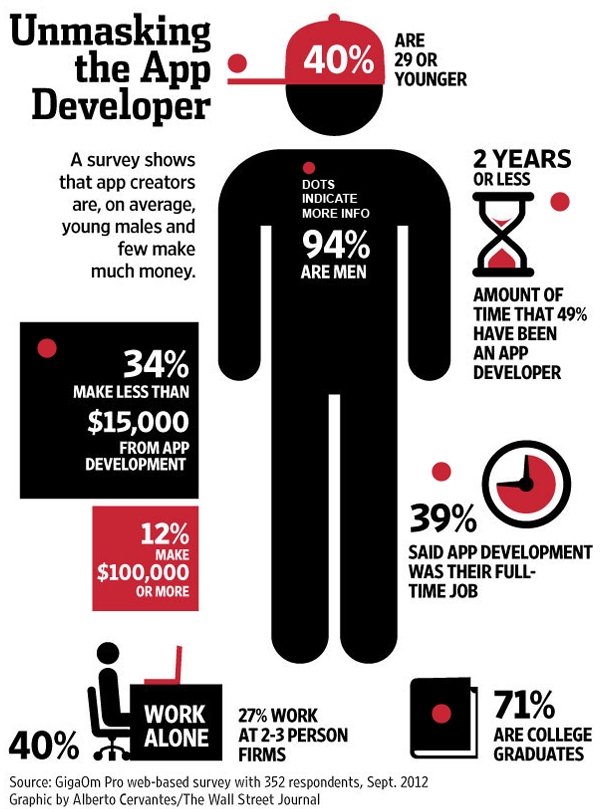

Nice infographic from the WSJ for their article on messaging apps – check it out here. They say that on average few app developers make much money, which was a surprise to me. Every startup I’ve worked with / talked to over the last 2 years routinely complains about a shortage of talent – mobile app development is particularly problematic because you have to develop for multiple platforms (iOS, Android, and to a lesser extent Windows, and Blackberry) you’re not just designing one web page accessible by any device.

“Everybody’s got to find their own way. Listening to me, maybe it’s fun, maybe it’s boring, who knows, you’re not going to succeed until you find your own way. I mean if you’re a musician you’ve got to find your own sound, your own way. Great musicians through history were the people who had their own madness, and were proud of their madness, especially if it was not what everybody else is doing. Well, the same is true of art, literature, politics, finance…especially finance. Yeah, you can copy other people, and many people do, that’s why everybody invests in the same thing, and that’s why it winds up being a bad investment. No, you’ve got to figure out your own way, no matter how absurd your way may sound, especially if your own way sounds absurd to others, you should pursue it even harder. You can learn from other people, but don’t try to be like Joe or Sally, try to be like yourself.” – Jim Rogers in Investor Guide

Found via Jim Rogers Blog

Interesting two part TechCrunch series about how the rise of crowdfunding is likely going to impact the business of venture capital and early stage investing.

Part I – Is Equity Crowdfunding A Threat To Venture Capitalists? (link)

Part II – The Crowd’s Money Can Dominate Early-Stage Investing, But Only If The VCs Get Their Cut (link)

![]()

Source: Intel, Found via The Big Picture

This morning Sir Richard Branson blogged about a glass bottom boat startup he loaned money to in the British Virgin Islands. The bulk of his short post is about the startup and his plans to continue to fund startups in the BVI.

What struck me most about his post was his first paragraph: “It takes gumption to become an entrepreneur. You need to show initiative, bravery and resourcefulness. You also need a lot of help along the way”

I’ve often thought about the most important qualities of an entrepreneur but to me, gumption might be the most important. It’s not always the smartest or most well funded that survive; it’s the shrewd, resourceful, and dedicated. While those qualities don’t guarantee success I would argue they’re fundamental to it.

You show me an entrepreneur who has made it without gumption and I’ll show you one lucky bastard.