After that last post about famous speculators and their speculations I have to balance things out a bit…

“For as long as I can remember, veteran businessmen and investors – I among them – have been warning about the dangers of irrational stock speculation and hammering away at the theme that stock certificates are deeds of ownership and not betting slips… The professional investor has no choice but to sit by quietly while the mob has its day, until the enthusiasm or panic of the speculators and non-professionals has been spent. He is not impatient, nor is he even in a very great hurry, for he is an investor, not a gambler or a speculator. The seeds of any bust are inherent in any boom that outstrips the pace of whatever solid factors gave it its impetus in the first place. There are no safeguards that can protect the emotional investor from himself.”

– J. Paul Getty

Found via Hussman

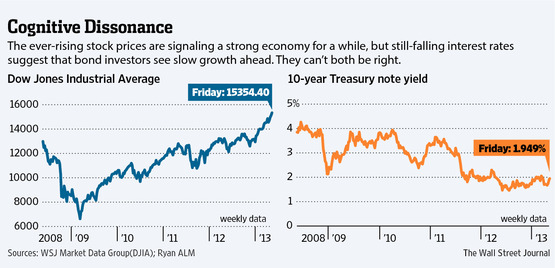

Naturally, Hussman’s broader market commentary is equally as thought provoking as the introductory quote above. He identifies two aspects of QE that are driving the stock market: (1) the pain of zero interest cash and (2) the superstition that QE removes downside risk.

This got me thinking about all the folks out there who feel they are “forced into equities” because they can’t find adequate returns elsewhere. Yes, thus far the outcome has been quite nice for those “forced” into the stock market but at some point there will be a correction. And at some further point the Fed is going to take the punch bowl away. So rather than sulk about cash’s paltry return, why not recognize the option value embedded in cash? It is essentially a put option on every asset in the world with no expiration. Yes it won’t feel very valuable when the stock market is setting records but it will when the market changes course. I would gladly accept a year or two of 0% to slightly negative real returns (cash today) if in a few years time I can safely find double digit annualized returns elsewhere; ESPECIALLY if the only other offer on the table carries such considerable downside risk (i.e. stocks & bonds today). Today this thinking / approach is as unpopular as it is boring: very.

Let’s end this post with the money shot from Hussman’s commentary (and please keep in mind price ≠ value):

In short, there is no transmission mechanism by which QE has any large and beneficial effect on the value of equities. There has certainly been an effect on price – but this effect is driven by the willingness of investors to abandon their demand for a risk premium that will actually compensate them for the risk they are taking.