A few days ago I stumbled upon a real gem – it was the key note speech to the Financial Analysts Federation Seminar at Rockford College on August 9, 1981 delivered by Dean Williams who was a Senior Vice President at Batterymarch Financial Management. The speech is called “Trying Too Hard” (link).

Dean lays out the idea that those in the investment management business are routinely trying too hard – there seems to be a vested interest in creating complexity as opposed to simplicity. He compares finance to physics in that if you learned enough about the laws that govern the physical (or financial) world you could extend your knowledge or influence over your environment. If you just worked hard enough – learned every detail about a company, discovered just the right variables for your forecasting models then earnings, prices, and interest rates would all behave in rational and predictable ways. Unfortunately, in the financial world (and sometimes in the physical world) things don’t play out in rational or predictable ways, no matter how much understanding you develop.

Humans are just not good at predicting things – what earnings will be in a few years, when interest rates will peak, what inflation will be. Most people in finance spend much of their time accumulating information to help make forecasts of all the things we have to predict. Dean concludes that confidence in a forecast rises with the amount of information that goes into it but the accuracy stays the same.

So does this mean all professional investors are categorically useless? No! The good news is you can be a successful investor without being a perpetual forecaster. Dean mentions one of the most liberating experiences you can have is to be asked to go over your firm’s economic outlook and say “We don’t have one”.

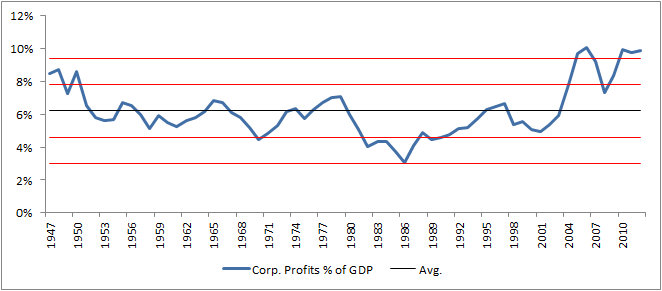

If there is a reliable and helpful principle at work in our markets its mean reversion – the tendency toward average profitability is a fundamental, if not the fundamental principle of competitive markets. It’s an inevitable force, pushing profits and valuations back to the average. This makes for a powerful investment tool. It can almost by itself select cheap portfolios and avoid expensive ones. The plain English equivalent Dean offers is “that something usually happens to keep both good news and bad news from going on forever”.

So besides having a healthy respect for mean reversion what other qualities can one bring to the table? He offers a few:

- Simple Approaches – he quotes Einstein as saying “most of the fundamental ideas of science are essentially simple and may, as a rule, be expressed in language comprehensive to everyone” and remarks that his own reaction was “sure, that’s easy for him to say” but as long as there are people out there who can beat professional investment managers using dart boards, he urges us all to respect the virtues of a simple investment plan

- Consistent Approaches – establish your approach and stick with it. He lists some of the top performing funds (circa 1981) and highlights the main thing they all had in common was the discipline to stick to their approach, to stay consistent

- Tolerance for the concept of “Nonsense” – or what the Zen call “Beginner’s Mind”. Expertise is great, but it has a bad side effect – it tends to create an inability to accept new ideas

- Spend your time measuring value instead of generating information – As mentioned before, most of us in finance spend our time gathering information and using it to make predictions. Dean advises us don’t forecast – buy whats cheap today; let other people deal with the odds against predicting the future

He goes on to mention an interesting study about man’s ability to forecast. A Wharton professor named J. Scott Armstrong published an article called “The Seer-Sucker Theory” where he collected studies of experts’ forecasts in finance, economics, psychology, medicine, sports and sociology. The summary of his findings is that expertise, beyond a minimal level is of little value in forecasting change. The punchline of his findings was “no matter how much evidence exists that seers do not exist, suckers will pay for the existence of seers”

***

That’s a very rough outline of the speech – it looks longer than it is and it’s quite an enjoyable read; if you liked what you read here then go read the whole thing (link).