The Absolute Return Letter: The Need for Wholesale Change

A good read about the state of the markets. Below you’ll find a hodgepodge of excerpts I found interesting – read the letter in its entirety for a more coherent argument. Note: everything you read below is a directly quoted excerpt.

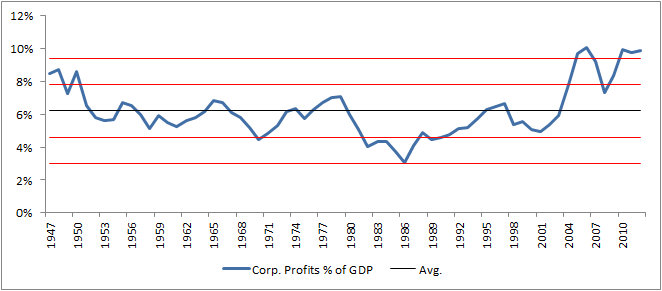

Intro & Chart:

On 5 March 2013 the Dow Jones Industrial Average set a new all-time high, surpassing

the previous high of 14,165.50, established back in October 2007. Only the stock

market doesn’t seem to recognise that the world is a very different place today when

compared to 5 ½ years ago. Many investors talk the bearish talk, yet they walk the

bullish walk. This apparent inconsistency is a function of the widespread belief that

central bank policy, whether emanating from Tokyo, Frankfurt, London or

Washington, provides an effective volatility hedge, allowing investors to ignore the

underlying economic and financial problems that continue to simmer. Chart 1 landed

in my inbox a few weeks ago, courtesy of Simon Hunt. A chart often says more than a

thousand words; it certainly does in this case.

Chart 1: Now and Then – 2013 vs. 2007

Source: Charles de Trenck, Transport Trackers. U.S. data unless otherwise indicated.

The Comedy Called Cyprus

I have long argued that the creation of the European Monetary Union was akin to

reintroducing the gold standard. The eurozone member countries are effectively

locked into a system very similar to the one that proved so hopelessly inadequate

during the great depression in the early 1930s. A monetary union is quite simply the

wrong model for a rapidly ageing Europe, but a combination of ignorance and

stubbornness means that those in charge refuse to see the writing on the wall.

The last couple of weeks have provided ample evidence that the political leadership in Europe is utterly clueless as to how to resolve the crisis. If there were any trust left between the public and our elected leaders that has now been unequivocally broken with the disastrous handling of the crisis in Cyprus.

It is a well known fact that European banks depend more on deposits for their funding requirements whereas U.S. banks tend to primarily use capital markets. The fact that European policymakers were prepared to sacrifice small depositors in Cyprus demonstrates a shocking lack of knowledge of this reality. How do they think depositors in other eurozone countries will interpret this blatant attack on private savings? At a time where banks need access to funding more than ever? An invisible line in the sand has been crossed and there is no way back. Next time a bank in a major eurozone country runs into serious difficulties, there is likely to be a bank run, primarily because the trust was broken with the shambolic handling of events in Cyprus. As outgoing BoE Governor Mervyn King once quipped (and Iparaphrase): “It is irrational to start a bank run but, once it gets going, it is perfectly rational to join in.”

Triffin’s Dilema

The chronic U.S. current account deficits of the 1950s and 1960s created a build-up of substantial U.S. dollar reserves in Europe and Asia just like now. Unlike now, however, the creditor nations would redeem those dollars for gold, depleting U.S. gold reserves to the point where they became

dangerously low. Today’s creditor nations redeem their dollars for U.S. Treasuries

instead.

With the U.S. off the gold standard, the ability for the government to honour its

obligations in gold is no longer an issue. It is instead the future purchasing power of

U.S. Treasuries that is at stake; hence the system is still intrinsically unstable.

An Emerging Dollar Bull Market?

Central bankers around the world are obviously aware of all these issues and this is where the story gets interesting. In central bank circles there is a growing realisation that monetary policy as prescribed over the past few years has become largely ineffective. The Bank of England buying another batch of gilts or the Fed acquiring yet more Treasuries has simply lost its va-va-voom.

Central bankers are therefore beginning to realise that they are running out of options in terms of propping up the global economy and something altogether different shall be required. It is in that light that the rumour mill is working overtime. Would it be far-fetched to expect a globally coordinated initiative whereby central banks step in with a groundbreaking new plan as to how the global economy and monetary system should be run?

For that to occur, our political leaders would have to be forced into a corner. That could only happen if the financial system became overwhelmed by yet another crisis. Policy makers simply won’t make the difficult decisions unless there is no other choice. Following that logic, central bankers actually have an interest in, and could do the world a favour by, ‘creating’ another financial crisis. Religiously targeting ZIRP is a good starting point. Near zero percent interest rates encourage risk taking to the extreme as we have seen over the past few years. Extreme risk taking leads to asset bubbles which will ultimately feed a crisis somewhere.

You may think that I have lost my marbles. I am not so sure. None of this is taken out of thin air. I have friends and acquaintances in many strange places around the world and this has come through one of the more trusted channels. Will it happen? I honestly don’t know but it is probably the best shot we’ll have at profoundly changing the monetary infrastructure of the world and for precisely that reason I hope it does happen.