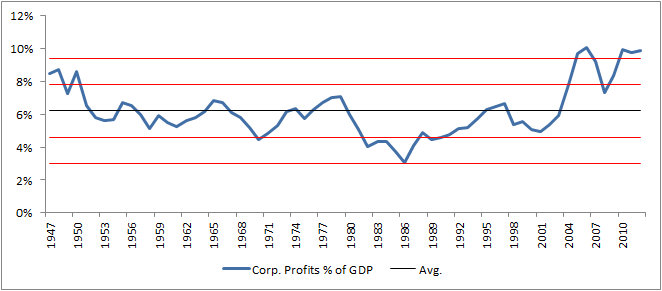

Below are a few excerpts from Tim Duy’s article about the strength of the economic recovery. Go check out the full article, charts included, here.

The economy has proved to be very resilient. We have weathered external demand shocks, external financial crises, and even fiscal contraction, and all the while economic activity continued to grind higher. Looking back, it seems that the biggest risk the economy faced was the Fed’s start/stop approach to quantitative easing. That problem appears solved with open-ended QE linked to economic guideposts.

At the risk of sounding overly optimistic, I am going to go out on a limb: The recovery is here to stay. Not “stay” as in “permanent.” I am not predicting the end of the business cycle. But “stay” until some point after the Federal Reserve begins to raise interest rates, which I don’t expect until 2015. This doesn’t mean you need to be happy about the pace of growth. But it does mean that a US recession in the next three years should be pretty far down on your list of concerns.

His take is based on strength in (1) industrial production, (2) retail sales, (3) the housing market, and (4) employment.

What does this mean for the market? Good question, nobody can be sure – but its certainly possible to see equities contract while the underlying economy continues to improve. Just read the previous posts highlighting John Hussman’s bearish take on the markets. Whatever the markets do, lets hope the economic recovery stays intact and at least provides a buoy should Mr. Market freak out.

Also, lets take into account the forward looking nature of equities, after all any real investor worrying about fundamentals should be thinking a minimum of 3-5 years out (despite the majority of Wall Street focusing on the next quarter or two). This will put fundamental / value investors in the uncomfortable position of factoring in the Fed’s exit well ahead of the rest of the market, if not already.

Tim’s bottom line:

Bottom Line: The US economy is less fragile than commonly believed; it has endured a series of shocks over the last three years without major incident. I am claiming neither that equity prices won’t stumble, nor that we should be happy with the pace of activity. But I do think that a recession is unlikely before the Federal Reserve begins raising interest rates – something not likely to happen for two years. While long-run predictions are dangerous, for the sake of argument add up to another two years for tighter policy to reverberate through the economy and you are looking at sometime around 2016/2017 when the next recession hits. That’s the timeframe I am currently thinking about.